In the first quarter of 2026, a shipment of high-count 80s yarn produced in northeastern Africa was loaded into containers at the port of Djibouti and shipped directly to Europe. The manufacturer was not a European mill, nor an Asian cotton-spinning giant, but the Ethiopian factory of Wuxi No.1 Cotton.

This delivery signals more than a 'first order': when Chinese-invested African mills export yarn to the EU with zero or reduced tariffs, the global trade flow of premium yarn is being redrawn.

The Location Advantage of African Capacity

Ethiopia sits on the East African plateau, close to the Red Sea and the Gulf of Aden. Sea freight time to major European ports is about 7 to 10 days shorter than from coastal China. Wuxi No.1 Cotton's choice of this location essentially trades geography for supply chain speed—European luxury apparel brands demand lead times measured in weeks, and African factories can offer a shorter delivery window than Asian counterparts.

More critically, Ethiopia enjoys the EU's 'Everything But Arms' (EBA) scheme, granting duty-free access for textile exports. For intermediate goods like yarn with thin margins, tariff savings translate directly into price competitiveness. Public customs data show that Chinese-made high-count yarn faces 8% to 12% import duties into the EU, while Ethiopian-made equivalents bypass this cost entirely.

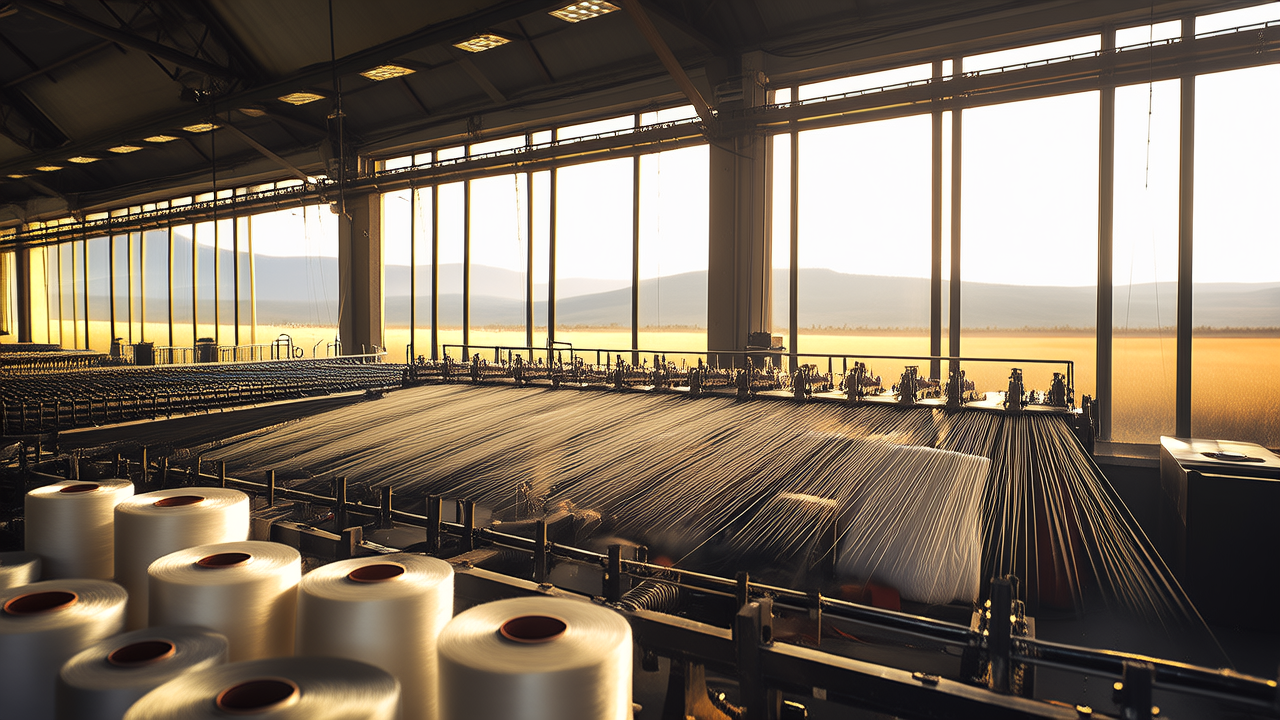

Asymmetric Competition in the High-Count Yarn Segment

The 80s yarn exported by Wuxi No.1 Cotton belongs to the high-count category, used primarily for premium shirts, bedding, and lightweight fabrics. This niche has long been dominated by Italian, Swiss, and select Chinese players, with entry barriers rooted in spinning precision and process stability.

Public information indicates that the Ethiopian factory has been expanding its high-count capacity and has already achieved bulk supply of 80s yarn to Pakistan. This means its products have passed technical validation in one of the world's most demanding cotton yarn markets. Having secured a foothold in Pakistan—a country that is the largest consumer of cotton yarn globally and notoriously picky about quality—the technical risk of entering Europe is significantly reduced.

For European buyers, sourcing high-count yarn from Africa is not a simple 'China replacement' but a strategic supply chain restructuring: identical quality, shorter transit time, lower tariffs, and reduced exposure to certain geopolitical risks. This combination of 'quality unchanged, cost optimized, delivery accelerated' is highly attractive in the current period of global textile supply chain reconfiguration.

The 'Africa Model' of Industry Chain Coordination

Wuxi No.1 Cotton's presence in Ethiopia extends beyond a single spinning project. According to industry disclosures, the company is spearheading the creation of a complete overseas textile and garment value chain, establishing supply-demand coordination mechanisms with local upstream and downstream enterprises. This suggests that yarn is only the first step, with potential subsequent phases involving weaving, dyeing, and even garment manufacturing.

This 'chain-based going-global' model differs fundamentally from earlier Chinese textile investments in Southeast Asia, which often involved isolated factories. In Ethiopia, cotton is partly sourced locally and from neighboring East African countries, then spun and directly linked to European brands, compressing intermediate links significantly. If dyeing and finishing capabilities can be established, future exports from Ethiopia to Europe could be fabric ready for cutting, not just yarn.

For European buyers exploring 'China+1' or 'China+Africa' sourcing strategies, this model offers a traceable and replicable supply chain blueprint.